Global Energy Report (2026)

The Infrastructure Paradigm Shift: From Reversible to Irreversible Decisions

.2e81242a.png&w=256&q=75)

Download the report: Global Energy Report (2026)

Executive Summary

If your infrastructure strategy was written before 2025, it is already out of date. In the old data center model, almost every decision was reversible—if you picked the wrong server generation, you refreshed it in three years. The entire discipline was built on the comfortable assumption that mistakes were depreciable and could be corrected in the next cycle.

The transition to gigawatt-scale AI infrastructure fundamentally destroys that model. When you commit to a generation strategy at gigawatt scale, you are placing a 20 to 40 year bet on a piece of infrastructure you cannot easily refresh, cannot easily move, and in many cases cannot easily exit. The operators who win the next decade will be the ones who understand that the most expensive mistake is the one you cannot take back.

The Financing Bottleneck and the Delay Tax

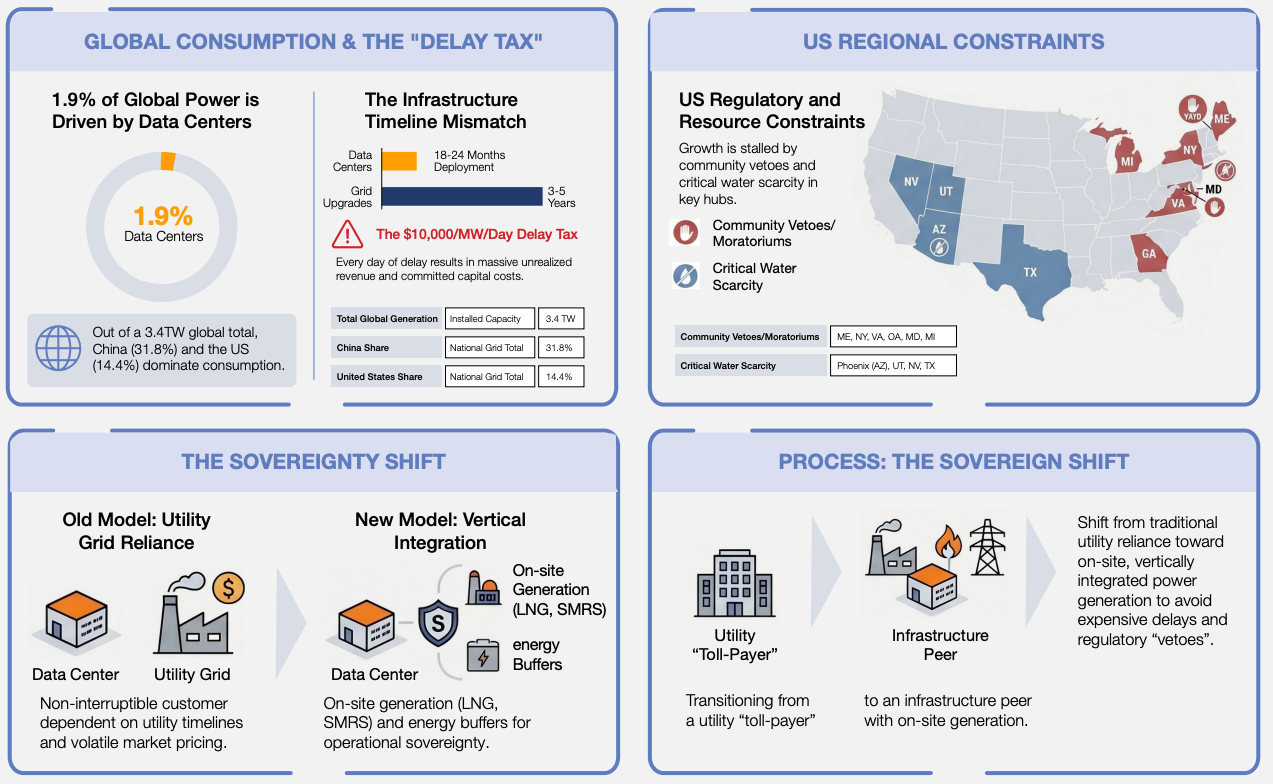

While grid interconnection queues frequently take the blame for stalled development, a deeper bottleneck lies in how projects are structured. The underlying constraint is that we are still trying to finance modern AI infrastructure using a model built for a very different generation of data center development. This mismatch creates massive unrealized costs. A 100MW deployment delayed by a year is not simply a project timeline problem. With the average lost revenue cost per MW per day at $10,000+, it represents a devastating financial penalty while demand migrates elsewhere. However, as recent federal FERC actions indicate, this bottleneck is no longer a static reality but a moving target as regulators attempt to force timeline updates.

A New Era of Constraints: Water and Workload Control

Furthermore, the constraints defining this infrastructure are multiplying. Five years ago the industry optimized primarily around power availability, but increasingly it has to optimize around power and water at the same time. A generation strategy that solves the power problem while creating a water problem is not actually solving the siting challenge.

At the same time, we are entering a period where the scarce asset is not compute or generation, but the control plane that decides when and where workloads run. As grids require flexibility and curtailment under stress, the true battle is over the interface—whether the grid operator, the hyperscaler, or the vendor gets to run the control loop for massive training clusters.

This report examines energy consumption by the world’s data centers. It accompanies two other major IDCA reports focused on Digital Readiness and Data Center development. This report identifies the energy stresses faced by nations, the use of sustainable energy in meeting demand, and how major data center operators and the nations in which they operate are addressing data center consumption. It does not make projections into the future, but does address scenarios that may face the industry. IDCA maintains research databases and related resources that can be brought to bear to create detailed country-by-country analyses and specific road maps for countries to use in developing optimal data center and AI hub plans, initiatives, and projects.

Insight

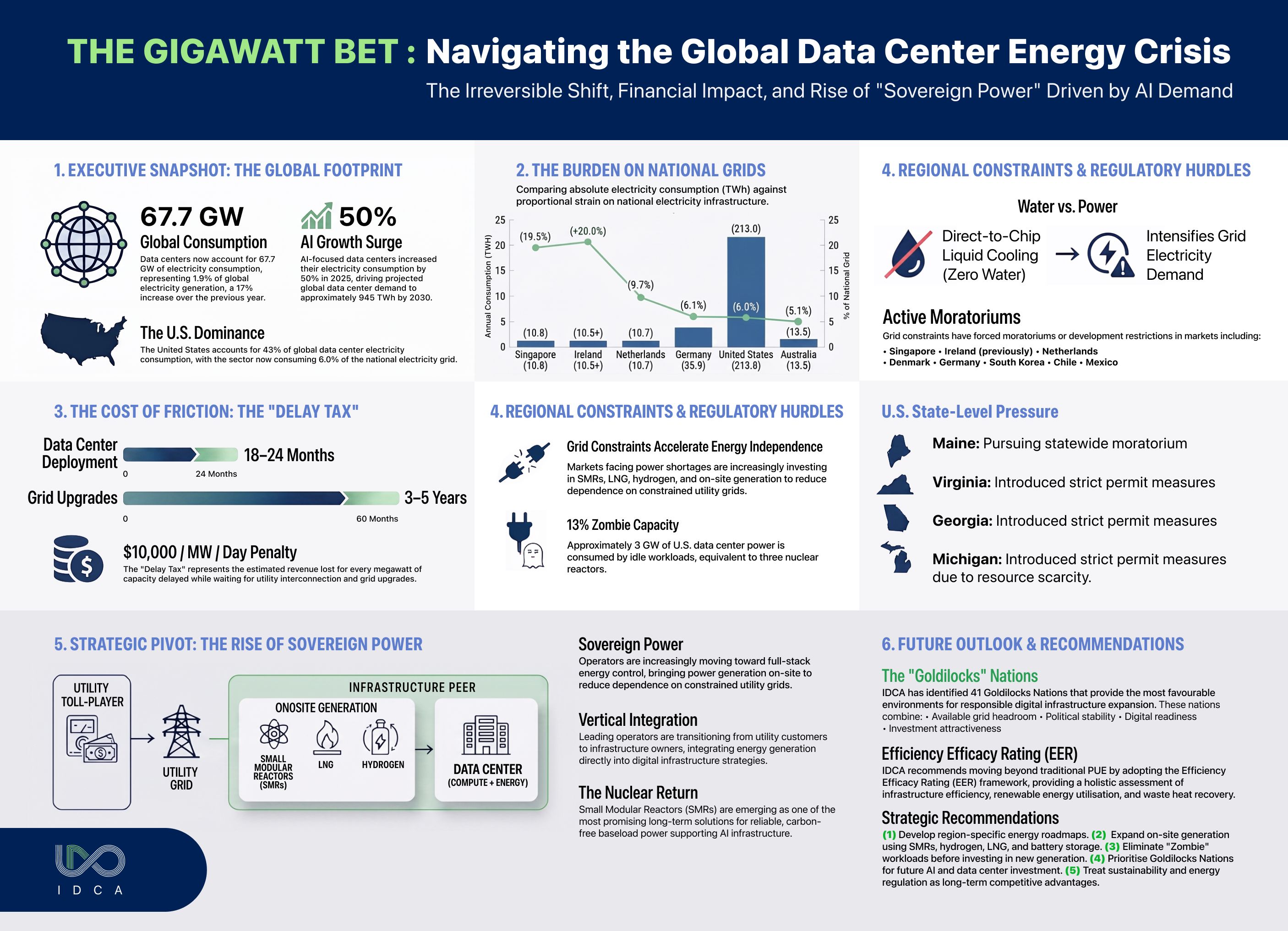

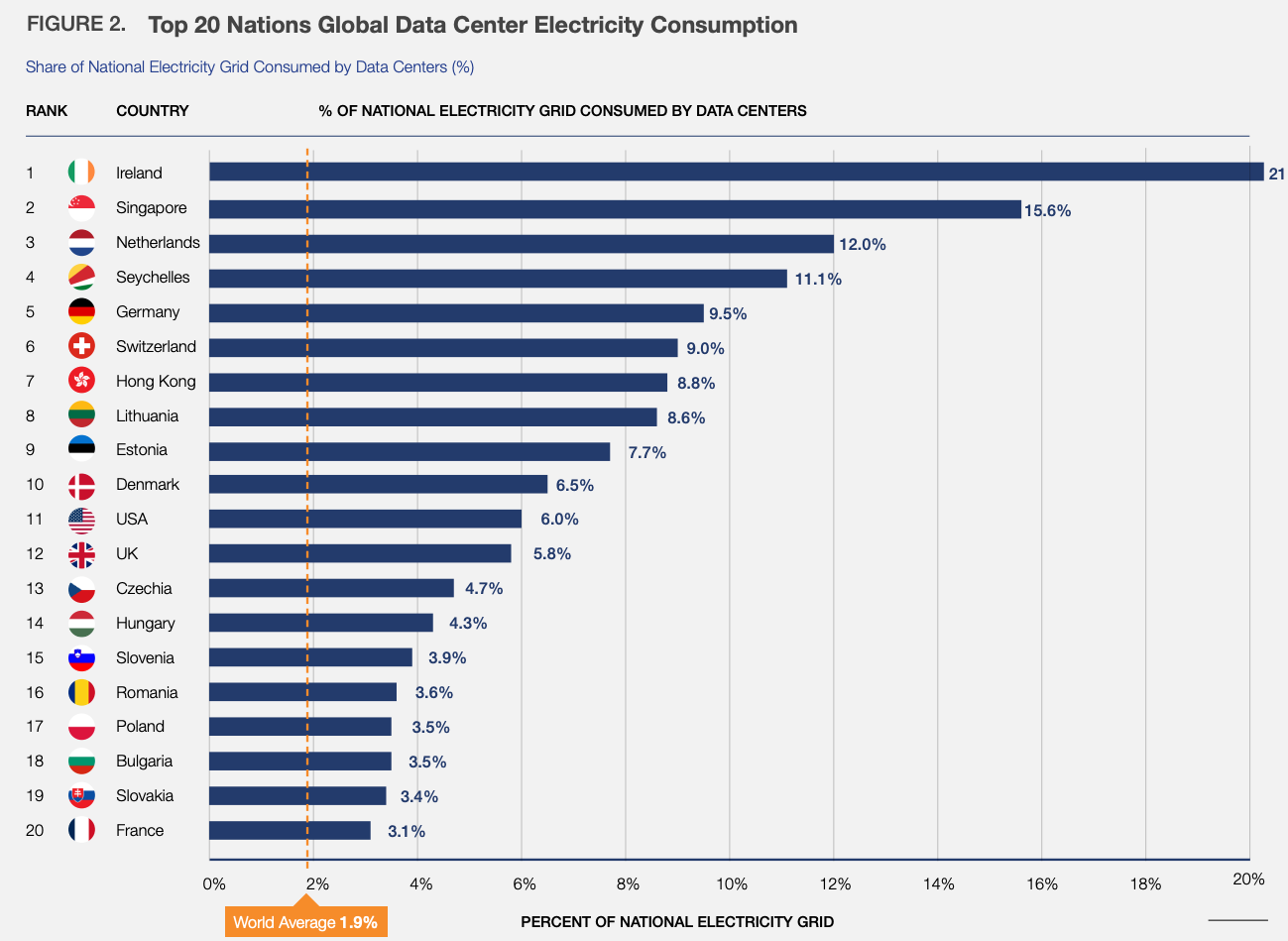

The world’s data centers now consume 67.7 gigawatts (GW) of electricity, representing 1.9% of global generation and a 17% increase over the prior year. The United States alone accounts for 43% of this total, with its data center footprint reaching 6.0% of the national grid. Artificial intelligence is fundamentally reshaping the trajectory of this growth: AI-focused data centers grew their electricity consumption by 50% in 2025, and global data center consumption is projected to reach approximately 945 TWh by 2030 (IEA, 2026), more than double today’s levels.

Key findings of this report include:

(1) Grid constraints are now critical in at least 12 major markets. While moratoriums are in place or under active consideration in Singapore, the Netherlands, Denmark, Germany, South Korea, Chile, and Mexico, Ireland recently ended its multi-year moratorium by mandating strict “bring your own power” and renewable energy obligations for all new facilities.

(2) The transition from evaporative cooling to closed-loop direct-to-chip liquid cooling eliminates on-site water stress but intensifies grid electricity demand, shifting the environmental burden from water systems to power infrastructure.

(3) An estimated 13% of U.S. data center power supports “zombie” applications, representing more than 3 GW of recoverable capacity equivalent to three nuclear reactors.

(4) Sustainable energy now supplies approximately 38% of global electricity generation, yet remains insufficient to meet accelerating data center demand; bridging strategies including Small Modular Reactors (SMRs), hydrogen fuel cells, liquefied natural gas (LNG), and Battery Energy Storage Systems (BESS) are being actively deployed.

(5) Twenty-seven developed nations possess sufficient grid headroom to absorb at least 1 GW of new data center capacity without new generation investment.

(6) IDCA has identified 41 “Goldilocks” nations that represent the most favorable environments for responsible digital infrastructure expansion.

The Shift to Sovereign Power and Vertical Integration As consumption scales and grid constraints tighten, relying entirely on external public utility timelines introduces a level of exposure that is increasingly difficult to manage. Consequently, successful operators are shifting toward full-stack control and Sovereign Power, bringing power under direct control through on-site generation and integrated campus designs. Crucially, this is no longer just an aggressive, contrarian developer strategy—it is now federally backed grid policy. Recent June 18 FERC orders have explicitly directed RTOs to build tariffs that accommodate co-location and behind-the-meter generation. The M&A logic is actively shifting toward vertical integration, where the goal is to deliver compute alongside energy rather than just traditional space and power.

The “Delay Tax” This strategic pivot is necessary because the friction between the rapid 18-to-24 month deployment timeline of a modern data center and the 3-to-5 year timeline required to upgrade community power lines is creating devastating developmental bottlenecks. This mismatch creates a massive “Delay Tax.” The average lost revenue cost of these delays is over $10,000 per megawatt, per day. However, this bottleneck is no longer a static reality but a moving federal target. Recent federal actions—specifically the June 18 FERC orders directed at major RTOs—are attempting to force tariff updates and streamline these interconnection delays, though the actual effects are currently projected rather than observed. When a 100MW deployment is delayed by just one year, the combination of lost revenue opportunity, cost of capital, and shifting demand can push the financial impact toward the billion-dollar mark.

The “Community Veto” and Legislative Pushback Inside the United States, this resistance has escalated into what is effectively a “Community Veto.” Local opposition is no longer just episodic friction; it is highly organized, armed with technical consultants, pre-written ordinance language, and heavily funded ratepayer coalitions. Fundamentally, this pushback is driven by cost allocation—residential ratepayers are fighting to avoid subsidizing the massive transmission and generation upgrades required by data centers. For example, Virginia is introducing a new rate class starting in January 2027 where data centers will be required to cover 85% of transmission and distribution costs and 60% of generation demand. Maine appears to be the first state moving a statewide data center moratorium through its legislature, and at least 11 other states—including New York, Virginia, Georgia, Maryland, and Michigan—have introduced similar stop-build or stop-permit measures.

Water as a Hard Regulatory Constraint Furthermore, the industry can no longer view the electrical grid as its only boundary. Water has transitioned from a simple efficiency metric into a hard regulatory constraint. In major development hubs like Northern Virginia, Phoenix, Utah, Nevada, and Texas, the availability of cooling water is starting to shape site selection almost as much as electrical capacity does. A generation strategy that solves the power problem while creating a localized water problem will fail; operators must now prove absolute water neutrality to survive community and regulatory scrutiny.

Data Center Electricity Consumption

Data centers in the United States consume 43% of the world total data center consumption, or 26.7GW. The collective footprint in the US has grown quickly over the past few years to reach 6.0% of the entire US electricity grids. This rapid growth has resulted in notable constraints in the Data Center Alley region of Northern Virginia, in California, and in a few other large hub areas, including Chicago and Dallas. A recent moratorium in Maine was vetoed by the state’s governor, but calls for moratoriums are being introduced in several state legislatures.

The current grid constraints are only the beginning, as artificial intelligence fundamentally alters the trajectory of digital infrastructure power consumption. According to recent projections, data centers could jump from consuming approximately 6% of U.S. power in 2025 to 12% by 2030, in the absence of significant new grid construction.

Trending Insights

IDCA News